|

241 18th Street South, Suite 415, Arlington, VA 22202

Telephone (805) 520-8350

www.avinc.com ● NASDAQ: AVAV

|

March 15, 2024

Ms. Beverly Singleton and Ms. Claire Erlanger

Division of Corporation Finance

Office of Manufacturing

United States Securities and Exchange Commission

100 F Street, N.E.

Washington, DC 20549

| Re: |

AeroVironment, Inc.

Form 10-K for the Fiscal Year Ended April 30, 2023

File No. 001-33261

|

Dear Ms. Singleton and Ms. Erlanger:

The following is in response to the comments of the staff (the “Staff”) of the Division of Corporation Finance of the Securities and Exchange Commission contained in the comment

letter dated February 26, 2024 pertaining to the Form 10-K for the fiscal year ended April 30, 2023 of AeroVironment, Inc. (the “Company”) filed on June 28, 2023. The Staff’s comments are repeated below (in bold-italics type) with the Company’s

response following (in regular type and updated disclosures in bold type).

Form 10-K for the Fiscal Year Ended April 30, 2023

Management’s Discussion and Analysis of Financial Condition and Results of Operations Critical Accounting Policies and Estimates

Goodwill, page 63

Goodwill, page 63

|

1.

|

We note your disclosure that subsequent to the performance of your annual goodwill impairment test, in May 2023 a

triggering event was identified that indicated that the carrying value of the MUAS reporting unit exceeded its fair value and that you recorded a $156 million goodwill impairment charge. We further note disclosure on page 59 under the heading

Impairment of Goodwill, that you determined that it was more likely than not that the fair value of the other reporting units were more than their carrying values as of the annual goodwill impairment test date. If you determined that the

estimated fair value substantially exceeds the carrying value for each of your reporting units, please disclose this determination. To the extent that the estimated fair value for any of your reporting units is not substantially in excess of

its carrying value and is potentially at risk of failing step one of your goodwill impairment analysis, please disclose (a) the percentage by which the fair value of the reporting unit exceeded the carrying value as of the date of the most

recent test; (b) discuss the degree of uncertainty associated with the key assumptions and (c) describe the potential events and/or changes in circumstance that could reasonably be expected to negatively affect the key assumptions used in

determining fair value. Please refer to Item 303(a)(3)(ii) of Regulation S-K and Section V of SEC Release No. 33-8350.

|

||

| The Company acknowledges the Staff’s comment and advises the Staff that the Company will revise all periodic reports of the Company filed pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), commencing with the quarterly report on Form 10-Q for the quarter ending January 27, 2024, which was filed on March 5, 2024 (the “Q3 2024 Form 10-Q”), to: | |||

| (1) |

Disclose management’s determination that the estimated fair value of each of the Company’s reporting units substantially exceeded its carrying value for any applicable reporting units. The following disclosure was included on page 37 of the Q3 2024 Form 10-Q: | ||

| During the most recent annual impairment test during the fourth quarter of fiscal year 2023, the estimated fair value of all reporting units, other than MUAS, substantially exceeded their carrying value. | |||

| (2) |

For the MUAS reporting unit, whose estimated fair value is not substantially in excess of its carrying value and is potentially at risk of failing step one of management’s goodwill impairment analysis, disclose the items described in (a) through (c) of the Staff’s comment. The following disclosure was included on page 37 of the Q3 2024 Form 10-Q: | ||

| The estimated fair value of the MUAS reporting unit does not substantially exceed its carrying value due to the impairment recorded during the most recent annual goodwill impairment test performed during the fourth quarter ended April 30, 2023, resulting in carrying value being equal to estimated fair value. Fair value determinations utilized in the quantitative goodwill impairment test require considerable judgment and are sensitive to changes in underlying assumptions, estimates, and market factors. Estimating the fair value of individual reporting units requires us to make assumptions and estimates regarding future plans, as well as industry, economic, and regulatory conditions. These assumptions and estimates include estimated future annual net cash flows, income tax rates, discount rates, growth rates, and other market factors. Estimated future annual net cash flows based in part upon our ability to obtain contracts from the U.S. D.o.D. and foreign allied nations and negotiate the estimated pricing are considered the most significant, sensitive assumptions. If current expectations of future growth rates and margins are not met, if market factors outside of our control, such as discount rates, income tax rates, or inflation, change, or if management’s expectations or plans otherwise change, including updates to long-term operating plans, then MUAS may become impaired in the future. Accordingly, the MUAS reporting unit is considered at an increased risk of failing future quantitative goodwill impairment tests. |

Results of Operations, page 64

| 2. |

We note your table presentation on page 65 of revenue, gross margin and adjusted operating income (loss) from operations generated by each reporting segment, along with your

discussion of revenue by product sales and contract services beginning on page 66. Please consider including a sub-table of revenue by product sales and contracted services, by segment, to enhance the overall narrative discussion of

changes in your revenue. In addition, consider providing a paragraph discussion of the reasons for the changes in profitability of each reporting segment.

|

|

| The Company acknowledges the Staff’s comment and advises the Staff that the Company will revise the referenced segment table to disclose revenue by product sales and contract services by segment and segment adjusted income from operations in all periodic reports of the Company filed pursuant to Section 13 or 15(d) of the Exchange Act, commencing with the Q3 2024 Form 10-Q. For reference, the below disclosure was included on page 38 and page 42 of the Q3 2024 Form 10-Q. | ||

|

||

| The Company also will revise the consolidated narrative discussion to include quantified reasons for changes in the Results of Operations to enhance

the overall narrative discussion, commencing with the Q3 |

2

| 2024 Form 10-Q. For reference, the below disclosure was included on page 39 of the Q3 2024 Form 10-Q, and corresponding disclosure for the nine-month period ended January 27, 2024 was included on pages 42-43 of the Q3 2024 Form 10-Q. Brackets have been added to indicate enhanced disclosures compared to similar disclosures in previous periodic reports. | ||

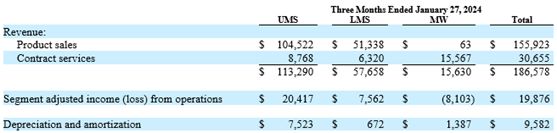

| Revenue. Revenue for the three months ended January 27, 2024 was $186.6 million, as compared to $134.4 million for the three months ended January 28, 2023, representing an increase of $52.2 million, or 39%. [The increase in revenue was due to an increase in product revenue of $64.7 million, partially offset by a decrease in service revenue of $12.5 million. The increase in product revenue was primarily due to an increase of $35.1 million from the production of our Switchblade products and an increase of $29.6 million of product deliveries of our UMS products, including $5.7 million associated with the recent Tomahawk acquisition. These increases were primarily driven by increased global demand for our unmanned systems associated with the current global conflicts as well as U.S. D.o.D. resupply. The decrease in service revenue was primarily due to a decrease of $11.5 million largely resulting from the closure of all COCO site locations during fiscal year 2023, a decrease of $4.3 million in customer funded R&D and engineering services due to a decrease in development programs in part due to delays in the establishment of the government fiscal year 2024 budget, partially offset by an increase of $4.3 million associated with the recent Tomahawk acquisition.] We expect the lower levels of UMS service revenues to continue through fiscal 2024 due to the closure of all COCO site locations during fiscal year 2023. With the higher backlog, the increase in the UMS product revenues as compared to the prior year period is expected to continue for the remainder of the fiscal year ending April 30, 2024. | ||

| Cost of Sales. Cost of sales for the three months ended January 27, 2024 was $119.3 million, as compared to $88.9 million for the three months ended January 28, 2023, representing an increase of $30.4 million, or 34%. The increase in cost of sales was a result of an increase in product cost of sales of $44.6 million, partially offset by a decrease in service costs of sales of $14.2 million. [The increase in product costs of sales was primarily due to an increase of approximately $39 million associated with the increase in product revenue and approximately $4 million due to a mix shift to a higher proportion of lower margin products driven by the increase in Switchblade production and an increase of $2.4 million in inventory reserve charges primarily due to the introduction of our next generation products. The decrease in service cost of sales was primarily due to a decrease in service revenue driven by a decrease of $13.1 million due to the closure of all COCO sites in the prior year. Cost of sales for the three months ended January 27, 2024 included $4.0 million of intangible amortization and other related non-cash purchase accounting expenses as compared to $3.3 million for the three months ended January 28, 2023.] As a percentage of revenue, cost of sales decreased from 66% to 64%, primarily due to an increase in the proportion of product revenue to total revenue and the prior year COCO operations costs, partially offset by a mix shift to lower margin products, resulting in an increase in gross margin from 34% to 36%. | ||

| In addition, the Company advises the Staff that the Company will provide disclosure regarding the change in profitability for each reporting segment for each period presented in all periodic reports of the Company filed pursuant to Section 13 or 15(d) of the Exchange Act, commencing with the Q3 2024 Form 10-Q. Such enhanced disclosure for each segment was included on pages 40-42 and 44-45 of the Q3 2024 Form 10-Q. For example, the enhanced disclosure for the UMS segment included on pages 40-41 of the Q3 2024 Form 10-Q is set forth below: |

3

|

||

| Revenue. UMS revenue for the three months ended January 27, 2024 was $113.3 million, as compared to $92.3 million for the three months ended January 28, 2023, representing an increase of $21.0 million, or 23%. The increase in revenue was due to an increase in product revenue of $29.6 million, partially offset by a decrease in service revenue of $8.6 million. The increase in product revenue was primarily due to an increase of $23.9 million largely resulting from increased product shipments of our Jump 20 and UGV product systems driven by increased global demand for our unmanned systems associated with the current global conflicts as well as U.S. D.o.D. resupply and $5.7 million associated with the recent Tomahawk acquisition. The decrease in service revenue was primarily due to decreases of $11.5 million from the closure of all COCO site locations during fiscal year 2023, partially offset by an increase of $4.3 million associated with the recent Tomahawk acquisition. | ||

| UMS Segment adjusted income from operations. UMS segment adjusted income from operations for the three months January 27, 2024 was $20.4 million, as compared to $11.8 million for the three months ended January 28, 2023, representing an increase of $8.6 million. The increase in UMS segment adjusted income from operations was primarily due to an increase of revenue of $21.0 million, partially offset by an increase of $7.9 million in cost of sales driven by increased sales volume of approximately $10 million, partially offset by a favorable sales mix of approximately $2 million primarily due to lower levels of COCO service revenue, partially offset by an increase in SG&A of $3.8 million driven by increased employee related expenses, partially offset by a decrease in intangible amortization of $2.4 million, and an in increase in R&D of $1.2 million due to development activities regarding enhanced capabilities for our products. |

Note 5. Intangibles, net, page 96

| 3. |

We note your disclosure that “due to the closure of all of the Company’s MUAS COCO sites during the three months ended April 30, 2023, we revised the estimated useful life for MUAS customer relationships which resulted in accelerated intangible amortization expense of $34,149,000 during the fiscal year ended April 30, 2023.” Given the $156 million goodwill impairment charge taken in the MUAS segment in the current year, tell us and disclose if the developed technology intangible asset acquired as part of the Arcturus acquisition and included in the MUAS segment was tested for impairment as of April 30, 2023. If not, please explain your basis for that decision. |

| The Company acknowledges the Staff’s comment and advises the Staff that the developed technology intangible asset acquired as part of the Arcturus acquisition and included in the MUAS segment was tested for impairment as of April 30, 2023. The Company intends to disclose that fact in its upcoming Annual Report on Form 10-K for the fiscal year ending April 30, 2024 and disclose any future impairment tests, as applicable, in corresponding Exchange Act periodic reports. | ||

| As background for the Staff, the developed technology intangible asset acquired as part of the Arcturus acquisition is utilized in the Company’s Jump 20 products. The MUAS segment historically used the Jump 20 products in both COCO services and product sales. The Company continues to market and sell Jump 20 products as part of product sales. The following describes the testing for impairment of the developed technology intangible asset acquired as part of the Arcturus acquisition as of April 30, 2023: |

4

|

MUAS customer relationship intangible asset

On February 24, 2023, the Company was issued a stop work notification for the Company’s remaining MUAS COCO services site location, which terminated the COCO flight services effective

immediately. The MUAS customer relationship intangible asset was directly associated with the Company’s COCO operations and relationship with the COCO site customer. Upon the closure of all COCO sites, the Company reevaluated the

estimated remaining useful life of the MUAS customer relationship intangible asset and determined that the remaining useful life was zero. Accordingly, the Company recorded accelerated amortization expense of $34,149,000 during the three

months ended April 30, 2023.

Annual goodwill impairment test

During the three months ended April 30, 2023, the Company performed its annual goodwill impairment test. The goodwill impairment test included a quantitative step 1 test in accordance with

ASC 350 for the MUAS reporting unit and reflected the impacts of the stop work notice. The estimated fair value of the MUAS reporting unit was determined to substantially exceed its carrying value.

Updated goodwill impairment test

Subsequent to the performance of the Company’s annual goodwill impairment test, in May 2023 a triggering event was identified that indicated that the carrying value of the MUAS reporting

unit exceeded its fair value. Specifically, the Company received notification that it was not down selected for a U.S. Department of Defense program of record, which resulted in a significant decrease in the projected future cash flows of

the MUAS reporting unit. As a result, the Company updated its estimates of long-term future cash flows used in the valuation of the MUAS reporting unit and performed an updated quantitative test for impairment. The Company first tested

the long-lived assets, including the acquired technology intangible asset, of the MUAS reporting unit (which is also the asset group) for recoverability in accordance with ASC 360. The asset recoverability test did not result in an

impairment. The Company then calculated the estimated fair value of the MUAS reporting unit in accordance with ASC 350, determining that it was less than its carrying value, which resulted in the recognition of a goodwill impairment

charge of $156.0 million.

Revised disclosure

The Company will revise its Note 5. Intangibles in its upcoming Annual Report on Form 10-K for the fiscal year ending April 30, 2024. Below is an example of the revised disclosure we

intend to include in the Form 10-K; brackets indicate additional disclosure:

Due to the closure of all of the Company’s MUAS COCO sites during the three months ended April 30, 2023, we revised the estimated useful life for MUAS customer

relationships, which resulted in accelerated intangible amortization expenses of $34,149,000 during the fiscal year ended April 30, 2023. [Additionally, in conjunction with the goodwill impairment test performed during the year ended

April 30, 2023, the remaining intangibles in the MUAS reporting unit were tested for recoverability. The asset recoverability test did not result in an impairment for the remaining intangibles in the MUAS reporting unit. Refer to Note

6—Goodwill for further details.]

|

Note 15. Income Taxes, page 107

| 4. |

Refer to your table presentation of deferred income tax assets and liabilities where we note the line item Section 174 Capitalization, resulting in a deferred tax asset of approximately $25

million at April 30, 2023. Please expand your disclosures to explain the meaning of this new deferred tax asset and its treatment for income tax accounting purposes. We note that revisions to Section 174 of the Internal Revenue Code, as

part of the 2017 Tax Cuts and Jobs Act, went into effect for tax years beginning after

|

5

|

|

||

| The Company acknowledges the Staff’s comment and advises the Staff that the Company will provide expanded disclosures to explain the meaning of Section 174 Capitalization and its treatment for income tax accounting purposes prospectively commencing with its upcoming Annual Report on Form 10-K for the fiscal year ending April 30, 2024. Below is an example of the expanded disclosures that we intend to include in our future filings. | ||

| For tax years beginning in 2022, the Tax Cuts and Jobs Act of 2017 (“TCJA”) eliminated the option to currently deduct research and experimental (“R&E”) expenditures in the period incurred and requires taxpayers to capitalize and amortize such expenditures over a period of five years (for U.S.-based research) or fifteen years (for non-U.S. based research), as applicable, pursuant to Section 174 of the Internal Revenue Code. As of April 30, 2023, the Company recorded a tax adjustment to capitalize and amortize its R&E costs, which resulted in an increase to income taxes payable of approximately $24,962,000 and a decrease to net deferred tax liabilities of a similar amount. | ||

| In addition, we will modify the description in the deferred income tax assets and liabilities table from “Section 174 Capitalization” to “Capitalized research and development costs.” |

Note 23. Segments, page 120

| 5. |

We note that your disclosure in Note 23 includes disclosure of gross margin, operating income and adjusted operating income (loss) by segment. Please tell us, and revise to disclose, the measure that is the profitability measure used by the CODM for purposes of making decisions about allocating resources to the segments and assessing performance. See ASC 280-10-50-27 through 28. Also, please revise to include disclosure of amounts that are included in the measure of segment profit or loss, such as depreciation and amortization, as required by ASC 280-10-50-22. Additionally, please note that the reconciliation required by ASC 280-10-50-30 in the footnotes is the total segment profit measure to your consolidated income before taxes for each year presented. Please revise accordingly. | |

| The Company acknowledges the Staff’s comment and advises the Staff that the Company will disclose that the profitability measure used by the CODM for purposes of making decisions about allocating resources to segments and assessing performance, as required by ASC 280-10-50-27 through 28, is adjusted operating income, defined as operating income before intangible amortization, amortization of purchase accounting adjustments, and acquisition related expenses, commencing with the Q3 2024 Form 10-Q. Such disclosure was included on page 32 of the Q3 2024 Form 10-Q: | ||

| Segment adjusted income (loss) from operations is the measure of profitability used by the CODM for purposes of making decisions about allocating resources to the segments and assessing performance. | ||

| The Company will revise the tables included in Note 23. Segments to disclose depreciation, depletion, and amortization expense and unusual items, as required by ASC 280-10-50-22, commencing with the Q3 2024 Form 10-Q. Such disclosure was included on page 32 of the Q3 2024 Form 10-Q: | ||

6

|

| The Company will also revise the tables included in Note 23. Segments to disclose the reconciliation of the total segment measure of profitability to the Company’s consolidated income before taxes, as required by ASC 280-10-50-30, for each period presented, commencing with the Q3 2024 Form 10-Q. Such disclosure was included on page 33 of the Q3 2024 Form 10-Q: | ||

|

Note 24. Geographic Information, page 122

| 6. |

We note your disclosure that sales to non-U.S. customers, including U.S. government foreign military sales in which an end user is a foreign government, accounted for 53%, 41% and 39% of revenue for each of the fiscal years ended April

30, 2023, 2022 and 2021, respectively. Please revise to disclose the amount of revenues from individual foreign countries, to the extent those amounts are material. See guidance in ASC 280-10- 50-41(a).

The Company acknowledges the Staff’s comment and advises that it has considered the guidance of ASC 280-10-50-41(a) and

determined that because revenues generated from external customers attributed to an individual foreign country are material, which the Company interprets to be in excess of 10% of its consolidated revenue, separate disclosure of any such

foreign revenues is required.

Fiscal year 2023

For the fiscal year ended April 30, 2023, Ukraine represented $100.1 million, or 18.5%, of the Company’s consolidated

revenues. Based on the guidance of ASC 280-10-50-41(a), disclosure of the revenue from the Company’s customers attributed to Ukraine is required to be separately disclosed, as the Company has concluded that such revenue is material for

Fiscal Year 2023. The Company’s international revenues from each of the remaining foreign countries (excluding Ukraine) were less than 10% of consolidated revenues for fiscal year 2023 and, therefore, the Company determined that revenue

from customers attributed to other countries was not material, based on guidance of ASC 280-10-50-41(a). The Company will separately disclose revenue from customers in foreign countries that account for 10% or more of total revenue with

disclosures of revenue by country in future filings.

|

7

|

Fiscal year 2022

The Company’s international revenues from customers in each foreign country were less than 10% of consolidated revenues for

fiscal year 2022 and, therefore, the Company determined that revenue from customers attributed to other countries was not material, based on guidance of ASC 280-10-50-41(a).

Fiscal year 2021

For the fiscal year ended April 30, 2021, Japan represented $42.4 million, or 10.7%, of the Company’s consolidated

revenues. Based on the guidance of ASC 280-10-50-41(a), disclosure of the revenue from the Company’s customers attributed to Japan is required to be separately disclosed, as the Company has concluded that such revenue is material for fiscal

year 2021. The Company’s international revenues from each of the remaining foreign countries (excluding Japan) were less than 10% of consolidated revenues for fiscal year 2021 and, therefore, the Company determined that revenue from

customers attributed to other countries was not material, based on guidance of ASC 280-10-50-41(a). The Company will separately disclose revenue from customers in any foreign countries that account for 10% or more of total revenue with

disclosures of revenue by country in future filings.

The Company will continue to monitor the significance of customer revenue by country and will disclose in future applicable

filings if revenues from customers attributed to an individual foreign country exceed 10% of the Company’s consolidated revenue or are otherwise deemed to be material.

|

The Company appreciates the efforts of the Staff in reviewing our response to the Staff Comment Letter. Should you have any questions regarding the Company’s response

to your comments, please do not hesitate to contact me at (805) 520-8350.

Sincerely,

AEROVIRONMENT, INC.

/s/ Kevin P. McDonnell

Kevin P. McDonnell

Senior Vice President and Chief Financial Officer

8